FAQs

Table Of Contents

- How does this study differ from the 2001 study?

- How significantly has the shale gas revolution changed the study’s perspective?

- What is AGF/AGA’s goal in releasing this study? What are you hoping to accomplish?

New Landscape For Natural Gas Supply And Price

- I thought natural gas in the United States was scarce. Where did all this natural gas come from?

- How much natural gas is the United States estimated to have and how much do we currently consume as a nation? Will we run out of natural gas soon?

- Will demand for natural gas increase and if so, at what rate? Will the production and supply of natural gas be able to increase at a similar rate?

- Is it possible that you’re underestimating shale well depletion rates?

- How do you expect natural gas’ share of U.S. power generation to change in the future?

- What are some of the potential uses for natural gas that have previously been overlooked?

- How will prices be impacted by an increase in demand for natural gas?

- What developing market trends are influencing the landscape for natural gas?

- How will future oil production impact natural gas production?

- How does the projected costs of crude oil, gasoline, and diesel fuel compare to that of natural gas?

Natural Gas and the Environment

- What environmental concerns exist around natural gas production?

- What emissions come from natural gas?

- Given the U.S. reliance on shale gas, how significant are the environmental concerns about hydraulic fracturing or “fracking?

- Given the gas-line accident in California, can you definitively say that natural gas is safe to use in my home?

- How environmentally friendly are natural gas vehicles?

Energy Security and Efficiency

- How will an increase in domestic production of natural gas impact LNG trade?

- How would exports impact the possibility for increased domestic natural gas use?

- What is the full fuel-cycle efficiency? How does the fuel cycle of natural gas compare to other fuel sources?

- Why is the full fuel-cycle important to consider?

- What is combined heat and power (CHP) generation? How is it more efficient than traditional generation?

- What are the benefits of using natural gas appliances?

Economic Impact and Contributions

- What new economic opportunities is natural gas creating?

- If we start exporting LNG, what will that mean to all these “economic opportunities”?

- What are the primary benefits of natural gas use in the residential and commercial sectors?

- On average, how much money can one save using natural gas appliances in their home?

- What is a local distribution company (LDC)?

- What are the core markets for gas LDCs?

- How does the role of LDCs differ between the power sector, industrial sector, and transportation sector?

- What are the main challenges facing LDCs with natural gas?

- How are LDCs helping to increase access to natural gas? What is their role?

- How easy is it for existing gas LDCs to add new customers?

- What are the barriers to growth and regulatory factors that inhibit the use of natural gas?

- What regulatory changes need to be made to get more natural gas use in homes, businesses and other parts of the economy?

- What local regulatory policies can help promote natural gas consumption?

- What type of public-private partnerships will be needed to promote the use of natural gas and restore American economic strength?

Natural Gas and Transportation

- Are natural gas vehicles (NGVs) more efficient than gasoline-fueled vehicles?

- How many NGVs are currently on the road, or in use, in the United States? How does that compare to NGV use in other countries?

- On average, how does the price of filling up a NGV compare to a gasoline counterpart?

- Are there incentives for consumers to purchase NGVs?

- Is it realistic to expect a widespread conversion to natural gas transportation?

- What policies are hindering the use of natural gas vehicles?

About the Study

How does this study differ from the 2001 study?

The 2001 “Fueling the Future” report update was a landmark study on the potential for market growth for natural gas that profoundly influenced the national conversation on energy policy. However, it was created at a time when conventional wisdom held that the United States was entering an era of natural gas scarcity. Since then, new technologies have changed our domestic energy industry, breathed new life into our economy and ultimately reshaped the course of our nation’s energy future. The new “Fueling the Future with Natural Gas: Bringing it Home” report reflects those changes, looking beyond conventional projections of natural gas demand and considering technologies and potential markets that, to date, have been overlooked or under-appreciated.

How significantly has the shale gas revolution changed the study’s perspective?

The natural gas revolution has upended long-held notions of natural gas supply and cost. Due to a process of combining hydraulic fracturing and horizontal drilling, the abundance of natural gas unlocked from these shale deposits and tight sandstone formations is sufficient to last at least 100 years at current rates of consumption. The U.S. energy landscape has forever been changed and in light of this, the trustees of the American Gas Foundation decided to revisit the landmark “Fueling the Future” study – updating its vision of demand growth for today’s energy landscape.

What is AGF/AGA’s goal in releasing this study? What are you hoping to accomplish?

First – amidst the considerable wealth of research, analysis and punditry that has surrounded the growth in natural gas supply, this new study aims to tell the local distribution company (LDC), or natural gas utility, story and discuss specific opportunities, across economic sectors, for greater and more efficient use of natural gas. This report is intended to serve as a resource for natural gas LDCs, their customers, regulators, legislators and other policy makers, industry, and the general public to use in understanding the new realities of the natural gas market. There is ample room for expansion of the domestic natural gas market, and our nation’s energy future will be built upon the foundation of our more than two million miles of natural gas pipelines. We must continue to tell the story of how the full journey of natural gas, from production to consumption, provides consumers with long-term and sustainable cost savings through its incredible efficiency.

Second – our current policies surrounding natural gas are outdated and were developed during a time when natural gas was perceived to be scarce. Our nation’s new reality of affordable, abundant natural gas requires new thinking and visionary policies. Regulations need to be revised to promote U.S. energy efficiency and support expansion efforts of natural gas utilities. This report calls for a collaborative relationship between American policymakers, communities, natural gas utilities, and customers to facilitate the creation of new markets and demand for this increasingly important fuel source. All Americans stand to gain if we make investments and update our policies now to realize the full potential of a natural gas-fueled future.

New Landscape for Natural Gas Supply and Price

I thought natural gas in the United States was scarce. Where did all this natural gas come from?

In the span of less than five years, “unconventional” technologies for natural gas development have changed the outlook for U.S. natural gas supply from scarcity to abundance. These “unconventional” technologies are major new advances in extraction technology in the oil and natural gas industry that allow access to resources not previously technically or economically recoverable.

In this report we focus on one category of “unconventionals”–natural gas that is produced using a combination of horizontal drilling and hydraulic fracturing–which creates pathways that allow the oil and natural gas to flow through dense rock into the wellbore. The process of combining hydraulic fracturing and horizontal drilling has gained widespread acceptance for its ability to successfully produce natural gas from less conventional hydrocarbon reservoirs. Together, these technologies now allow commercial production from formations so tight that gas had been unable to escape from them over millions of years.

How much natural gas is the United States estimated to have and how much do we currently consume as a nation? Will we run out of natural gas soon?

In recent years, estimates of the technically recoverable resource natural gas base have ranged from 2,300 – 3,800 trillion cubic feet (Tcf), enough to supply current consumption for 88 – 154 years. By 2012 shale gas accounted for 39 percent of U.S. lower-48 production and IHS CERA expects that it will account for 58 percent of total productive capacity by 2035. Unconventional gas from all sources (shale, tight sands, coal bed methane, and associated gas from unconventional oil plays) is expected to provide 90 percent of total natural gas productive capacity by 2035.

For 2012, the U.S. Energy Information Administration detailed how the 25.5 trillion cubic feet of natural gas consumed is used by end use. Out of that annual total, 23.4 trillion cubic feet was delivered to consumers in the following sector amounts:

-

Residential: 4.179 trillion

-

Commercial: 2.9 trillion

-

Industrial: 7.1 trillion

-

Vehicle Fuel: 32 billion

-

Electric Power: 9.1 trillion

Will demand for natural gas increase and if so, at what rate? Will the production and supply of natural gas be able to increase at a similar rate?

Because so much unconventional natural gas is now available, the U.S. natural gas resource base can now accommodate significant increases in demand without requiring a significantly higher price to elicit new supply. For the next decade, domestic natural gas supplies are expected to be sufficiently robust to meet substantial growth in demand across all sectors. The country has experienced a transformational shift in the perceived role of natural gas—from an energy source sometimes seen as unreliable and scarce 10 years ago, to one that is now recognized as an essential component of a clean and secure energy portfolio. Natural gas will heat our homes, run our vehicles, generate electricity and partner with renewable energy sources for decades to come.

Is it possible that you’re underestimating shale well depletion rates?

Unconventional technology is steadily improving natural gas production economics. Because unconventional production techniques such as horizontal drilling and hydraulic fracturing allow greater access to the reservoir by a single well, the productivity of unconventional gas wells is much higher on average than that of conventional natural gas wells. As producers have gained experience, each well and each play has been developed more quickly and with better performance characteristics than its predecessor.

How do you expect natural gas’ share of U.S. power generation to change in the future?

The largest projected growth in natural gas demand will occur in the power sector as natural gas generation fills the gap left by retiring coal units and also serves new electric load. Natural gas consumption by the electric power sector is expected to almost double from current levels by 2035.

What are some of the potential uses for natural gas that have previously been overlooked?

The many new possibilities for natural gas use span all sectors of the economy and include conversions from oil heat to natural gas and electricity to natural gas for space heat, water heat, and cooking. Using natural gas as a power generator as some coal capacity is phased out has increased consumption. Also, integrating new renewable capacity into the generation fleet and adding compressed natural gas (CNG) and liquefied natural gas (LNG) automobiles, vans, trucks, transportation fleets, locomotives, barges, and ships has increased consumption. In addition to these uses, new innovative uses have been created, including, microgrids that can provide small scale power and combined heat and power which produces electricity and heat from a single source of energy at the site of use, achieving high overall energy efficiency.

How will prices be impacted by an increase in demand for natural gas?

Thanks to unconventional technologies, extensive volumes of natural gas can now be economically developed in the United States while prices remain relatively low and stable. IHS CERA estimates that about 900 trillion cubic feet (Tcf) of unconventional gas resources—more than one-third of the total recoverable resource base—can be produced economically at a Henry Hub price between $3.75 and $4.25 per thousand cubic feet (Mcf). As a result, we expect natural gas prices to remain in the $4-5 per MMBtu (constant 2012 $) on an annual average over the long term, albeit with some short-term cyclicality.

What developing market trends are influencing the landscape for natural gas?

Companies have taken time to respond to the new demand opportunities resulting from the unconventional natural gas revolution, but the expectation is now for significant growth in gas demand for power generation, industrial use, transportation, and LNG exports.

U.S. industrial natural gas demand is reversing a long-term decline in response to the growing availability of low-cost natural gas and natural gas liquids (NGLs). The three largest users of natural gas in the industrial sector include the chemicals, petroleum refining and food industries. The abundance and outlook for sustained affordable prices of natural gas have game-changing implications for power generation, increasing market share for natural gas-fired generators and resetting the cost and environmental benchmarks for new generation capacity additions.

Market potential for natural gas in transportation is quite large and significant penetration of natural gas into the vehicle market remains a long-term prospect. Of the 230 million light-duty vehicles on the road in 2012, only an estimated 100,000 were fueled with natural gas.

How will future oil production impact natural gas production?

The transfer of unconventional natural gas technology to oil plays has unlocked a new crude oil resource base that had previously been uneconomic. Since 2008, the U.S. has led the world in the growth of new supplies of crude oil. Production of unconventional “tight” oil has increased from 100,000 barrels per day in 2003 to an estimated 2 million barrels per day (mbd) in 2012. The rapid increase in tight oil production has also led to a substantial increase in natural gas that is associated with the primary oil production.

How does the projected costs of crude oil, gasoline, and diesel fuel compare to that of natural gas?

The price of crude oil is projected to remain around $90 per barrel (constant 2012 $). Natural gas equivalent per barrel is approximately $16, meaning that natural gas will be 3- 4 times cheaper than oil for decades to come.

For vehicles, the projected retail costs of gasoline and diesel fuel will be approximately twice the natural gas price on a Btu-equivalent. Such a sustained price differential will help to increase the attractiveness of natural gas as a transportation fuel.

Natural Gas and the Environment

What environmental concerns exist around natural gas production?

The benefits of developing the abundant and clean natural gas energy resource in America can and should be realized in a safe and responsible manner. The production of natural gas has been done safely for more than 60 years. Impacts on local communities, water management and disposal, and greenhouse gas emissions are manageable with prudent development and with the use of best practices in well construction and completion. These issues require industry involvement with local communities and with federal, state, and local regulators.

What emissions come from natural gas?

One of the greatest benefits of natural gas from an environmental perspective is that it results in the lowest CO2 emissions of any fossil fuel. When used to generate electricity, natural gas emits as much as 50 percent less CO2 than coal. In addition, natural gas use results in negligible emissions of sulfur dioxide (SO2), nitrogen oxides, mercury, and particulates compared with other fuels.

Emissions from natural gas utility distribution systems have dropped 16 percent since 1990, even as the number of customers served has increased by 30 percent. Only 0.3 percent of produced natural gas is emitted from systems operated by local natural gas utilities according to data from U. S. Energy Information Agency and the U. S. Environmental Protection Agency. Continued efforts to upgrade and modernize the natural gas pipeline network to enhance safety are lowering emissions even further.

Given the U.S. reliance on shale gas, how significant are the environmental concerns about hydraulic fracturing or “fracking"?

The benefits of developing the abundant and clean natural gas energy resource in America can and should be realized in a safe and responsible manner. Natural gas produced with the aid of hydraulic fracturing is a clean source of energy and can be extracted safely, while protecting our environment, and a framework of regulation exists at the state level that helps to address safety and environmental concerns associated with hydraulic fracturing. The incremental rules put in place over the past few years have not slowed growth in drilling and production, supporting the view that reasonable regulations are not likely to materially inhibit hydrocarbon supply in North America.

Given the gas-line accident in California, can you definitively say that natural gas is safe to use in my home?

Safety is the number one priority for the natural gas distribution and transmission industry. According to the U.S. Pipeline and Hazardous Materials Safety Administration, our domestic abundance of clean natural gas is delivered via the safest energy delivery system in the nation. Safety is a joint effort – a partnership that engages customers, regulators and policymakers at every level, and natural gas utilities and pipelines undertake a wide range of pipeline integrity, pipeline safety and public education programs.

There is significant oversight and regulation focused on the natural gas industry to help ensure public safety, and the design, construction, operation, inspection and maintenance of all operating pipelines are subject to state and federal regulations and requirements. The U.S. Department of Transportation’s Pipeline and Hazardous Materials Safety Administration (PHMSA) establishes federal safety standards for pipelines, and PHMSA partners with state pipeline safety agencies on inspections and enforcement of intrastate pipelines. Individual states can regulate intrastate pipeline systems above and beyond federal requirements, and there are hundreds of state specific pipeline safety regulations currently in place.

The natural gas industry invests billions of dollars each year to help ensure that natural gas is delivered safely and efficiently through the 2.4 million miles of U.S. natural gas pipelines.

How environmentally friendly are natural gas vehicles?

Natural gas vehicles produce 20 to 30 percent lower greenhouse gas emissions at the tailpipe than comparable gasoline or diesel vehicles. In the passenger car segment, natural gas vehicle’s tailpipe emissions are lower than those of a comparably sized and styled plug-in hybrid or a battery electric vehicle using electricity produced from coal.

Energy Security and Efficiency

How will an increase in domestic production of natural gas impact LNG trade?

The increase in domestic energy production has opened the dialogue about U.S. exports of natural gas rather than large-scale imports of natural gas that were anticipated just a few years ago. Our nation’s domestic abundance of natural gas has opened the door for wise and efficient growth of natural gas consumption, including potential LNG exports, while maintaining relatively low and stable prices. When the U.S. contributes to global LNG supplies, gas-consuming countries will have more supply options, reducing the market power of previously dominant suppliers. Additionally, increasing domestic oil production will reduce U.S. demand for oil imports and could relieve pressure on world oil prices.

How would exports impact the possibility for increased domestic natural gas use?

The North American gas resource base is so extensive that it could accommodate a significant increase in production to support higher demand, including LNG export projects, without the need to access resources that are significantly higher cost. This means demand can grow considerably without materially affecting long-term prices, estimated to remain between $4–5 per million Btu (MMBtu) through 2035. This dynamic holds for any increase in demand for U.S. natural gas—not just from LNG export projects.

IHS CERA’s analysis of the domestic market effects of U.S. LNG exports suggests that exports will not significantly affect U.S. natural gas prices and consequently, will not depress demand. A study delivered in December 2012 by NERA Economic Consulting concluded that exports could increase domestic gas prices a small amount from zero to $1.11 per Mcf.

What is the full fuel-cycle efficiency? How does the fuel cycle of natural gas compare to other fuel sources?

The “full fuel-cycle” efficiency takes into account the total energy required to produce and deliver natural gas or electricity to the appliance. Many appliance efficiency standards only consider the energy consumed on site. This means that all the losses that occur “upstream” – between the fuel production and the end use – aren’t counted.

The natural gas journey, from wellhead to burner tip is 92 percent efficient, using approximately 8 percent to produce, process, and deliver natural gas to end users.

The loss is much greater for electricity. Although there is a wide variation across regions, on a national average in 2012, electric generation used 60 percent of its energy input to produce and deliver fuel to the power plant, to generate electricity, and deliver it to end users.

Why is the full fuel-cycle important to consider?

To realize the full benefits of natural gas, we need to rethink how we measure energy efficiency. While appliance efficiency labels report site efficiency, full fuel-cycle efficiency is a better and more accurate measure of energy efficiency because it includes the energy required to produce and deliver the power to the appliance. As only 8 percent of natural gas energy is lost as it makes the trip from wellhead to burner tip, a natural gas appliance will have a full fuel cycle efficiency that is about 92 percent efficient. Electric generation uses 60 percent of its energy input to produce and deliver fuel to the power plant. Measured on a full-fuel cycle basis, an electric appliance has only about 40 percent of its site efficiency.

This full fuel-cycle enables a more comprehensive analysis of the total energy and emissions impacts of a particular fuel source, allowing for better understanding of its energy and environmental impacts.

What is combined heat and power (CHP) generation? How is it more efficient than traditional generation?

Combined heat and power generation (CHP), also known as cogeneration, produces electricity and useable heat from a single source of energy at the site of use, achieving high overall energy efficiency and avoiding the losses and costs associated with transmission and distribution from the central power grid. Natural gas is the fuel of choice for existing CHP installations, with 71 percent of capacity consuming 3.4 Bcf per day of gas.

What are the benefits of using natural gas appliances?

From a full fuel-cycle perspective, using natural gas appliances is more energy efficient than using electric appliances. Also, because the already large disparity between retail natural gas prices and retail electricity prices is expected to widen over time, increasing gas’s share of these markets can increase cost efficiency. In addition, with the prospect that natural gas prices will be significantly lower than electricity prices in many regions over the long term, the life-cycle cost of natural gas appliances can be lower than that of their electric counterparts.

Economic Impact and Contributions

What new economic opportunities is natural gas creating?

The new outlook for natural gas cost and availability is increasingly contributing jobs and revenues to the economy at the national, state and local levels. By 2035, the natural gas exploration and development supply chain is expected to contribute 3.5 million jobs, $475 billion in value added to U.S. GDP and nearly $125 billion in government revenues to the U.S. economy. In addition, the impact of natural gas on manufacturing has stimulated job and economic growth, increasing our nation’s competitiveness. It is estimated that international companies will invest at least $50 billion through the end of the decade on projects that take advantage of low-price natural gas here in the United States.

In addition, natural gas has created an increase in real disposable income for households of approximately $1,200 in 2012, which will steadily increase to $2,000 in 2015 and grow to more than $3,500 by 2025 in addition to increasing real GDP 2 percent to 3.2 percent per year ($500 - $600 billion) through 2035.

The expected low cost of natural gas coupled with more varied uses will result in lower energy and transportation costs for consumers. IHS CERA projects residential natural gas rates to be almost four times lower than residential electricity rates by 2030, and that natural gas will be three to four times cheaper than oil for decades to come.

If we start exporting LNG, what will that mean to all these “economic opportunities”?

The natural gas market today is characterized by abundant supply and significant potential for expanding its use in homes, businesses, power generation, industrial plants, and vehicles; as well as the export of liquefied natural gas. Investments in these energy applications can provide benefits to our nation’s economy, environment and national security. Conversely, increases in demand also support the long term economic viability of domestic natural gas production.

AGA believes that there is room to grow smart use of natural gas at reasonable and relatively stable prices. These strong natural gas supply fundamentals along with a robust and reliable natural gas delivery infrastructure suggest that over the next decade, a range of demand scenarios can be met by a diverse and responsive supply market within an estimated price band of $4.00 to $6.50 per MMBtu—a level well below the peak market prices of the preceding decade. Even significant increases in demand may be supported by this large, dynamic, robust and diverse North American natural gas resource base. When coupled with expanding infrastructure and appropriate regulatory constructs, we envision relative natural gas market stability during the next ten years and possibly beyond.

Additionally, a December 2012 study by NERA Economic Consulting concluded that U.S. LNG exports would unambiguously benefit the U.S. economy finding that the higher the volume of LNG exports, the greater the net economic benefit.

What are the primary benefits of natural gas use in the residential and commercial sectors?

The primary benefits of natural gas use in the residential and commercial sectors are higher energy efficiency and lower energy costs. In terms of full fuel-cycle efficiency, natural gas appliances generally have an advantage over electric appliances owing to the very large amounts of energy required to produce and deliver electricity. Further, residential electricity rates are expected to be almost four times as high as residential natural gas rates on a national average by 2030. In most regions the outlook for an increasingly large divergence between retail natural gas and retail electricity prices can make a conversion to natural gas a cost effective means of increasing energy efficiency for some appliances.

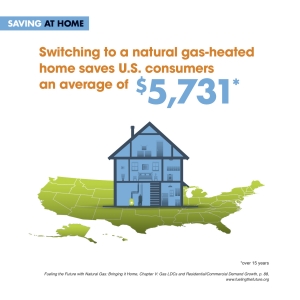

On average, how much money can one save using natural gas appliances in their home?

According to the American Gas Association, low domestic prices of natural gas have led to savings of almost $35 billion for residential natural gas customers over the past three years. Households that use natural gas appliances for heating, water heating, cooking and clothes drying spend an average of $654 less per year than homes using electricity for those applications. These savings are achieved not just through the comparatively low price point of natural gas, but also due to the efficiency of the delivery network operated by natural gas utilities.

Natural gas utilities are committed to helping customers achieve even greater energy savings by investing heavily in energy efficiency programs. In 2011, natural gas utilities created total savings of more than $300 million for customers – about $107 per household – and offset 6.5 million metric tons of carbon dioxide through energy efficiency programs.

The Role of Gas LDCs

What is a local distribution company (LDC)?

A local distribution company, or LDC, is a regulated local gas utility that delivers natural gas from a pipeline system through the local distribution company to homes and businesses. There are more than 1,200 gas local distribution companies in the United States that are investor-owned, municipally-owned or owned by co-operatives. Gas LDC services, rates and facilities are regulated by 49 public utility commissions or by their municipal or co-operative owners.

What are the core markets for gas LDCs?

Local distribution companies serve more than 65 million residential customers, more than five million commercial customers and more than 190,000 industrial and power generation customers.

How does the role of LDCs differ between the power sector, industrial sector, and transportation sector?

Most industrial and power sector natural gas customers receive their natural gas deliveries from natural gas LDCs. Approximately 95 percent of industrial gas customers and 69 percent of power sector customers receive natural gas deliveries on gas LDC systems; however, these customers tend to be small as natural gas LDC deliveries accounted for only 53 percent of industrial gas volumes and 26 percent of gas volumes used by power sector customers. In other words, although the volume of customers in these sectors is high, the volume of natural gas used by them is small.

Natural gas utilities’ role in the transportation sector is currently limited, but the prospect of expanded use of natural gas powered vehicles creates the potential for the role of local distribution companies to grow in building and supplying residential refueling stations for natural gas vehicles.

What are the main challenges facing LDCs with natural gas?

Regulation and infrastructure expansion will be the largest challenges facing local distribution companies. In order for these growth opportunities to be possible, policy reform is required to remove economic barriers and promote energy efficiency through the use of natural gas.

How are LDCs helping to increase access to natural gas? What is their role?

Natural gas utilities have an important role in helping ensure natural gas use is expanded. Natural gas utilities can educate new and existing customers on the overall, long-term benefits of using natural gas, which will help promote a more receptive environment for system expansion and increase awareness of the additional opportunities to use natural gas in homes and businesses.

Many gas LDCs are taking a leading role in promoting a more receptive environment for system expansion, but they cannot accomplish that task on their own. With public utility commission support, natural gas LDCs can provide additional value by serving growing natural gas markets such as new industrial and power customers and by supplying LNG and CNG to natural gas vehicle refueling stations.

How easy is it for existing gas LDCs to add new customers?

Natural gas utility growth occurs through increased natural gas sales to existing customers or through connecting supplies to new customers. Because adding new customers to an existing LDC system requires new infrastructure, there are typically higher costs for the utility than when connecting new customers. Constructing new infrastructure also requires additional approvals and regulations, which can slow down the expansion process.

Regulatory Perspectives

What are the barriers to growth and regulatory factors that inhibit the use of natural gas?

Barriers to growth for increased natural gas use include recovering the often high upfront costs of investments by natural gas utilities and consumers; conflicting federal, state, and local policy objectives; regulations grounded in outdated assumptions regarding natural gas supply and cost; and developing a consensus as to the new realities of the natural gas market.

What regulatory changes need to be made to get more natural gas use in homes, businesses and other parts of the economy?

Many existing natural gas regulations were developed during a time when natural gas was perceived to be scarce and market fundamentals were different than they are today. Re-evaluating the natural gas regulatory structure can help identify new opportunities for natural gas utilities and their customers.

Governments should promote natural gas system expansion as part of a comprehensive energy strategy and such policies for system expansion, appliance codes and standards development, energy efficiency programs and R&D funding should be reexamined based on the current and future market realities.

Governments should authorize public utility commissions to allow system expansion costs to be recovered through general tariffs applied to new and existing customers, and also provide explicit subsidies—economic development grants or state-backed bonds—for expansion of natural gas networks to underserved areas that meet established density criteria.

What local regulatory policies can help promote natural gas consumption?

State governments and public utility commissions should consider adopting policies that promote the use of full fuel-cycle energy efficiency, full fuel-cycle emissions standards and full-cycle cost analyses. Such analyses would encourage the increased use of natural gas and extend natural gas service to new customers. In addition, both public utility commissions and local governments should promote system expansion and allow costs of expansion to be recovered by local distribution companies.

Examples of states currently pursuing policies of this kind are:

-

In New York, St. Lawrence Gas has launched a system expansion using not only a temporary contribution in aid of construction from new customers, but also funding from county, regional and state governments. These funds include property tax reductions as well as direct grants.

-

Currently, only about 31 percent of homes in Connecticut have natural gas heat; the typical oil-heat customer spends about $2,650 a year on fuel and the typical gas customer spends just $1,100. The Governor and the legislature believe that fuel conversion will create jobs, make in-state business more competitive, and improve the environment. The Governor’s energy plan has set a target of 300,000 new natural gas customers.

-

Mississippi has adopted an explicit policy of encouraging expansion of the state’s natural gas infrastructure in order to draw industry investment and promote economic development. The state’s Public Service Commission recently approved a Supplemental Growth Rider permitting one of its gas LDCs to spend up to $5 million annually on system expansion to support industrial projects. These funds can be used to fill the gap between actual expansion costs and “economic” costs. The cost of this supplemental investment is spread across all gas LDC customers, with a permitted rate of return of 12 percent.

What type of public-private partnerships will be needed to promote the use of natural gas and restore American economic strength?

Natural gas utilities require regulatory and legislative support to promote a more receptive environment for expanded natural gas use. Natural gas utilities and public utility commissions should develop partnerships with customers, builders, utilities and economic development agencies to update existing regulations related to energy efficiency and system expansion.

Infrastructure

Are there plans to expand the existing natural gas pipeline infrastructure?

America’s natural gas utilities safely and reliably deliver natural gas to 65 million customers per year through 2.4 million miles of pipeline. The pipeline grid has excess capacity throughout the center of the continent and has delivery constraints to the coasts, especially in the U.S. Northwest, Northeast, and Southeast. With the major growth market for natural gas going forward, significant natural gas infrastructure additions will be required. New pipelines and other infrastructure projects are being constructed to eliminate pipeline bottlenecks and deliver natural gas from new supply basins into growing market areas.

Building an economic business case for expanding natural gas service into sparely populated areas is often challenging for natural gas utilities. One potential solution is to develop proposals that combine a modest residential and commercial load with a large industrial customer. In Maine, gas LDCs are expanding their systems to deliver natural gas to serve paper mills and, with the industrial demand providing a base level of support for the infrastructure, are also connecting residential and commercial customers along the way.

Natural Gas and Transportation

Are natural gas vehicles (NGVs) more efficient than gasoline-fueled vehicles?

Natural gas vehicles produce 20 to 30 percent lower greenhouse gas emissions at the tailpipe than comparable gasoline or diesel vehicles. In the passenger car segment, natural gas vehicle’s tailpipe emissions are lower than those of a comparably sized and styled plug-in hybrid or a battery electric vehicle using electricity produced from other fossil fuels.

How many NGVs are currently on the road, or in use, in the United States? How does that compare to NGV use in other countries?

There are about 140,000 NGVs on U.S. roads today and more than 15 million worldwide. Other parts of the world are realizing the potential of natural gas vehicles and moving forward. There are 1.8 million natural gas vehicles and Europe, 4.4 million in South America and 8.8 million in Asia and the Middle East. Natural gas provides only about 0.2 percent of the energy consumed in the transportation sector.

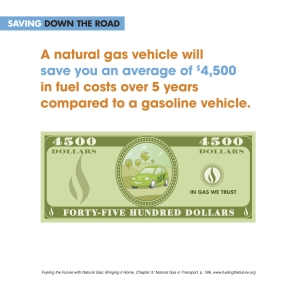

On average, how does the price of filling up a NGV compare to a gasoline counterpart?

As a transportation fuel, natural gas currently costs from $1.50 to $2.00 less per gasoline gallon equivalent than gasoline.

Are there incentives for consumers to purchase NGVs?

A number of states offer tax incentives to encourage the purchase of natural gas vehicles. A complete list of current state tax incentives for alternative fueled vehicles, including NGVs, is provide by the U.S. Department of Energy and can be found at http://www.afdc.energy.gov/laws/.

Although there are no federal tax incentives for NGVs, the Federal Corporate Average Fuel Standards provide incentive multipliers for alternative fuel vehicles. Fuel economy multipliers are revenue neutral to the government and vehicle manufacturers are more likely to be influenced by these types of incentives than by tax incentives, manufacturing grants or loan guarantees.

Is it realistic to expect a widespread conversion to natural gas transportation?

The market potential for natural gas in transportation is quite large and significant penetration of natural gas into the vehicle market remains a long-term prospect. The sustained gap between natural gas and oil prices provide an opportunity for natural gas to progress from niche fuel to key contributor in this sector. Although up-front costs are higher for natural gas vehicles than for conventional vehicles, fuel savings over the life of the vehicle can pay back the higher capital costs over a period of years.

Transportation companies are adding compressed natural gas (CNG) and liquefied natural gas (LNG) automobiles, vans and trucks to their fleets, and considering the use of LNG in locomotives, barges and ships. City fleets are recognizing the value of using more natural gas, both because of its environmental benefits as well the fuels lower cost. They are doing so by transitioning buses, taxis and event waste management trucks to run on natural gas.

What policies are hindering the use of natural gas vehicles?

Regulations need to be re-evaluated to remove impediments to natural gas use in transport. For example, some bridges and tunnels prohibit the transport of LNG while diesel fuel is allowed. Supply is also handled according to the original intention of its use. LNG produced in peak shavers is treated differently from other LNG (for example, it may not be exported) although it is the same physical product.

The tax structure for competing fuels needs to be rationalized. Both LNG and diesel are taxed on a per-gallon basis, rather than on a diesel-equivalent basis. This places LNG at a significant disadvantage considering that its energy density is lower than that of diesel—a gallon of LNG has a lower Btu content than a gallon of diesel. As a result, LNG is taxed 71 percent higher than diesel fuel. The economics of LNG versus diesel look compelling even with this additional tax burden, but taxing the two fuels equally will improve LNG’s economics even further. CNG and gasoline are already taxed according to energy content (on the basis of a gallon of gasoline-equivalent).